You've probably done some version of this already. You saved photos of inset cabinets, compared quartz colors, maybe walked through your kitchen and mentally removed a wall or moved an island. Then the practical question shows up fast. How do you finance a kitchen renovation without making the whole project feel risky?

That question comes up constantly in South Jersey, especially in places like Cherry Hill, Haddonfield, Moorestown, Voorhees, and Medford where homes often have solid long-term value, but kitchen scopes can vary wildly. One household needs a focused refresh to improve function. Another is planning a full redesign with cabinetry, layout changes, lighting, and finish upgrades. The money side should follow that scope, not the other way around.

A good finance kitchen renovation plan starts with reality. You need a budget that matches the kind of kitchen you're building, a funding option that fits your timeline, and a payment plan that protects you while the work is underway. When that part is handled early, design decisions get easier because you're choosing with guardrails instead of guessing.

Table of Contents

- Create a Realistic Budget for Your South Jersey Kitchen

- Compare Kitchen Renovation Financing Options

- Prepare Your Lender Application for Fast Approval

- Manage Project Payments and Contingency Funds

- Maximize Your Renovation's Return on Investment

- Your Kitchen Financing Plan from Start to Finish

Create a Realistic Budget for Your South Jersey Kitchen

The biggest early mistake is shopping for financing before you know what kind of project you're funding. A kitchen that keeps the same footprint behaves very differently from one that adds custom storage, moves plumbing, or opens into another room.

Start with scope, not the loan

A useful national benchmark comes from a 2025 Hanley Wood Market Intelligence study, which found that a minor kitchen remodel averaged $28,458, a major midrange remodel averaged $82,793, and an upscale remodel averaged $164,104, as cited by NerdWallet's kitchen remodel cost guide. That spread is the clearest reminder that “kitchen remodel” isn't one price category.

In South Jersey, homeowners usually land in one of three practical buckets:

- Minor refresh that improves appearance and daily use without major layout work

- Midrange remodel with meaningful upgrades to cabinetry, surfaces, appliances, and function

- High-end redesign with major trade coordination, premium finishes, and deeper structural or layout decisions

Practical rule: If your project changes the footprint, adds trade complexity, or pushes into custom detailing, your financing needs to be planned with more breathing room than a cosmetic upgrade.

Turn a wish list into a working budget

A realistic budget isn't just a total number. It's a breakdown of what's driving cost. In actual kitchen planning, the biggest swings usually come from cabinetry, countertop material, appliance level, electrical scope, plumbing changes, flooring transitions, tile work, and whether walls or windows are changing.

Before talking to a lender, it helps to organize your monthly obligations and renovation priorities in one place. A simple household expenses tracker can help you see what payment range feels comfortable before you commit to anything.

Then get a preliminary project estimate based on your actual kitchen, not a generic online calculator. A detailed kitchen remodeling cost breakdown is helpful because it translates broad categories into line items homeowners can react to. That's where a vague goal like “update the kitchen” becomes something concrete such as “keep the layout, replace the cabinets, upgrade lighting, and spend more on storage than on moving plumbing.”

Use that estimate to separate must-haves from nice-to-haves. If budget pressure shows up, the smartest cuts usually come from scope complexity, not from stripping out every finish you care about.

Compare Kitchen Renovation Financing Options

Once you know the rough project scope, the funding conversation gets clearer. The right tool depends less on what's trendy and more on how the job unfolds, how long you expect to stay in the house, and whether you want flexibility or payment certainty.

A strong baseline comes from Upstart's summary of kitchen remodel financing, which cites Harvard JCHS data showing 76% of home improvement projects were funded primarily with cash or savings, while 15% of kitchen and bath spending used home equity financing. That supports what many homeowners experience in practice. Smaller jobs are often paid from liquid funds, while larger jobs tend to move toward equity-based borrowing.

Kitchen Financing Options at a Glance

| Financing Option | Best For | Interest Rate | Pros | Cons |

|---|---|---|---|---|

| Cash or savings | Smaller remodels and homeowners who want no loan payment | Varies by your opportunity cost | No lender process, no monthly debt, simple | Reduces liquidity and emergency reserves |

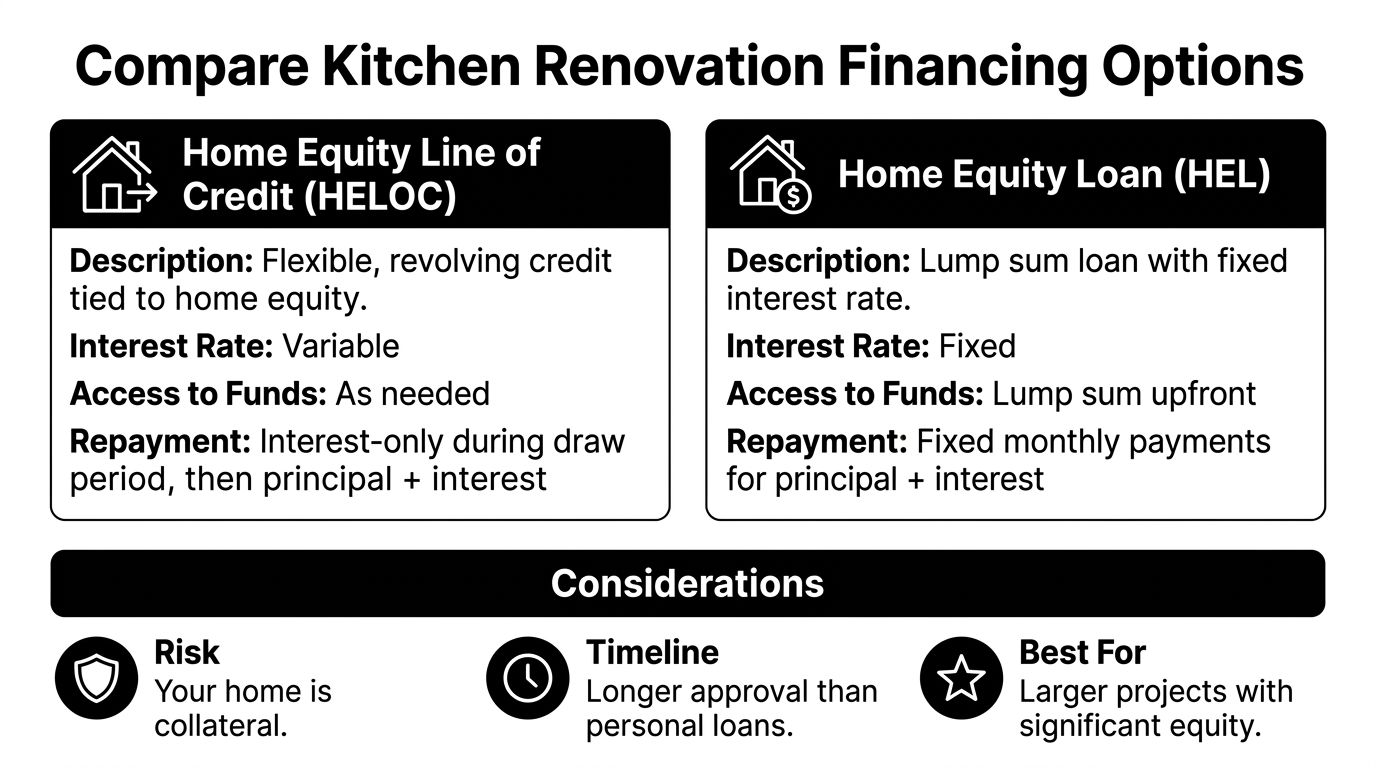

| Home equity loan | Larger one-time projects with a defined budget | Usually fixed | Predictable payment, lump sum funding | Your home is collateral, less flexible if scope changes |

| HELOC | Phased jobs or remodels where timing and draws may change | Usually variable | Flexible access to funds, useful for staged spending | Payment can change, your home is collateral |

| Personal loan | Homeowners who want speed or don't want to use home equity | Often fixed | Fast approval, no home collateral | Monthly payment may feel tighter on bigger scopes |

| Cash-out refinance | Large projects when mortgage restructuring also makes sense | Depends on mortgage terms | Can consolidate financing into one mortgage | More paperwork, closing costs, resets mortgage structure |

| Credit card or promo financing | Very small purchases or tightly controlled short-term balances | Variable or promo | Convenient for appliances or a limited purchase | Risky if the balance lingers past the promo period |

| Contractor-arranged financing | Homeowners comparing convenience with direct lender options | Varies by program | Streamlined process, project-focused | Terms need close review |

How each option behaves in real projects

A home equity loan works best when the budget is fairly settled. If the plan, materials, and labor scope are already defined, the fixed structure is easier to live with because the payment won't move around while the kitchen is under construction.

A HELOC fits projects with some moving parts. That might include a remodel where homeowners are doing the kitchen first and a mudroom or pantry later, or where finish selections are still being finalized. The flexibility is valuable, but variable payments can become uncomfortable if you're already stretching to reach the upper end of your comfort zone.

A personal loan makes more sense than many people assume. Some homeowners in South Jersey don't want to tie a kitchen project to the house at all. That can be especially appealing if they want to preserve home equity flexibility or avoid touching an existing mortgage structure. A financing page such as kitchen remodel finance options can help you compare project-based lending against traditional bank products.

A cash-out refinance deserves more caution than it gets in casual renovation talk. It can work, but only when the larger mortgage picture makes sense too. If you're evaluating that route, a practical resource on how to choose a cash-out refinance partner can help you compare lenders and ask better questions about fees, timing, and fit.

Home equity products usually make the most sense when the project's useful life is long and the budget is too large to force through a short repayment window comfortably.

There's another local reality worth naming. Financing isn't only for households that can't pay cash. BuyFin's renovation financing discussion notes that 65% of homeowners with incomes over $150,000 still use financing for major renovations. In practice, that often comes down to preserving liquidity, keeping reserves available, and choosing where cash should stay parked while the remodel is underway.

What usually doesn't work is mismatch. A small cosmetic update financed with a large equity product can be more cumbersome than necessary. A major redesign funded with a short-term unsecured payment that feels tight every month can create stress that follows the project long after installation is done.

Prepare Your Lender Application for Fast Approval

Good applications move faster because the numbers and paperwork line up with the project story. Lenders want to know what you're borrowing for, what it will cost, and whether your income and obligations support the payment.

What lenders usually want to see

Most lenders look for stable income, a manageable overall debt picture, and documentation that supports the amount requested. They also want to see that the renovation budget is grounded in a real estimate rather than a rough guess scribbled from internet averages.

That's one reason clean project planning matters so much. If your estimate shows cabinetry, countertops, installation, finishes, and related labor in a way that makes sense, underwriting tends to go more smoothly than when the scope is vague.

A useful mindset shift helps here. Financing a remodel doesn't signal financial weakness. As noted earlier, higher-income homeowners often borrow by choice to preserve cash. The smoother path is being organized.

Build a clean application package

Bring these items together before you apply:

- Income records such as pay stubs, W-2s, tax returns, or other documents your lender requests

- Asset statements for checking, savings, brokerage, or retirement accounts if the lender wants a broader financial picture

- Debt details including current mortgage information and recurring loan obligations

- Property information that confirms ownership and occupancy

- Project estimate from a contractor or design-build team that shows the intended scope clearly

- Photo references or plans if your lender asks for more detail on the renovation

Application tip: A lender can't underwrite a moving target very well. If you're still changing the kitchen from week to week, pause and settle the scope first.

For homeowners who want a quick refresher on how preapproval logic works, even though it's mortgage-focused, Superior Credit Repair explains mortgage preapproval in a way that helps clarify what lenders are trying to verify.

This short video also gives homeowners a useful overview before they start gathering documents:

The practical goal is simple. Make it easy for the lender to understand both your finances and your renovation plan. When those two pieces support each other, approval tends to be less frustrating.

Manage Project Payments and Contingency Funds

Getting approved isn't the finish line. The way you release funds during the remodel has a direct impact on stress, change orders, and whether the project stays financially healthy.

Use a payment schedule tied to work completed

A kitchen remodel should have a written payment schedule that connects draws to real milestones. Deposits, progress payments, material ordering, installation stages, and final payment should all be spelled out before work starts.

That protects both sides. The contractor has clarity on timing and purchasing. You have clarity on what triggers each payment and what deliverables should be in place first.

A sound schedule usually works better than either extreme. Paying almost everything up front creates risk for the homeowner. Holding back too much can slow ordering, scheduling, and trade coordination.

Consider putting these items in writing:

- Milestone definitions tied to specific work completed, not vague dates

- Change order process showing who approves added cost and when payment is due

- Allowances and selections so you know what happens if you choose materials above the original budget

- Final walk-through terms that define punch-list completion before the last payment

Keep contingency money separate and protected

Contingency money deserves its own lane. Don't blend it mentally with your base contract amount. Once demolition starts, hidden conditions, electrical updates, or finish revisions can appear, and you want those choices to come from planned reserves rather than panic.

A separate contingency fund gives you decision-making room. Without it, every surprise feels like a crisis.

Lien waivers are another point homeowners often miss. If your project involves multiple trades or suppliers, ask how lien waivers are handled as payments are made. This helps confirm that parties who've been paid can't later claim they weren't.

If you're coordinating a remodel with several moving parts, guidance on how to manage contractors during a renovation can help you keep communication, scheduling, and payment expectations aligned.

A finance kitchen renovation plan only works when the money remains visible all the way through the job. Approved funds can still be mishandled if payment timing is loose, paperwork is unclear, or contingency money gets spent on upgrades too early.

Maximize Your Renovation's Return on Investment

Homeowners usually ask two ROI questions. First, “Will this kitchen add value?” Second, “If I'm borrowing for it, am I making a smart move?” Those are related, but they aren't identical.

What usually earns back more

The strongest lesson from the data is that bigger spending doesn't automatically create better financial return. Jake N Finance Group's summary of kitchen remodel stats notes that Zillow reports a major midrange kitchen remodel has an ROI of about 51%, while other data suggests minor remodels can recoup 85% or more. That's a meaningful gap.

For South Jersey homeowners, that usually points toward upgrades that are visible, functional, and broadly appealing:

- Cabinet improvements that increase storage and clean up the room visually

- Countertop and surface updates that modernize the kitchen without requiring full reconstruction

- Lighting and hardware changes that sharpen the finished look

- Appliance and workflow upgrades that improve daily use

A focused budget kitchen upgrades guide can help sort high-impact changes from expensive changes that don't necessarily return much.

Borrow for the scope that solves real problems and stays legible to the next buyer. That usually beats overbuilding for a hypothetical buyer profile.

Should you finance if you may sell soon

If a sale may happen soon, financing can still make sense, but the reason matters. If you expect a full dollar-for-dollar recapture, you may be disappointed. If you want the kitchen to sell more smoothly, photograph better, compete better locally, or feel better during the time you still live there, the calculation is different.

Minor and mid-scope improvements often fit that situation better than a deep custom overhaul. They refresh the space, reduce buyer objections, and avoid loading a pre-sale timeline with the cost and complexity of a major redesign.

There's also a recordkeeping point homeowners should remember. Keep contracts, invoices, and proof of payment. Renovation spending may affect your home's cost basis, and your tax professional can advise you on what documentation matters for your situation.

Your Kitchen Financing Plan from Start to Finish

A solid kitchen financing plan isn't built around a loan product first. It starts with a clear scope, a usable preliminary estimate, and an honest look at how the payment will fit into your household finances.

From there, the choices get simpler. Match the funding method to the project size and timeline. Prepare the lender file with organized documents and a clean estimate. During construction, release money by milestone, protect your contingency funds, and keep all approvals in writing. Finally, measure the project against likely return, especially if a sale may be on the horizon.

That's the part many homeowners in South Jersey find reassuring. This process is manageable when each decision follows the last one in order. You don't need to solve the entire remodel in one sitting. You need the right first step, then the right next one.

If you're ready to start with actual numbers instead of rough guesses, review the financing details at The Cabinet Coach financing page and use that as the basis for a more grounded renovation plan.

If you're planning to finance a kitchen renovation in South Jersey, the smartest move is to begin with a real project scope and a realistic estimate. The Cabinet Coach offers a mobile, design-focused process that helps homeowners turn ideas into a workable kitchen plan, material selections, and a preliminary budget they can use when evaluating financing.