You’re probably in one of two places right now. Either you’ve been staring at an older kitchen in Cherry Hill, Haddonfield, Moorestown, or Medford and thinking, “We need to do this,” or you’ve already picked out cabinet colors, countertop samples, and appliance ideas, then hit the hard question. How are we paying for it?

That pause is normal. In South Jersey, a lot of kitchens sit inside older homes with quirks hidden behind walls, tired layouts, and finishes that no longer fit how families live. The excitement is real, but so is the financial tension. A remodel can improve daily life and help resale, but only if the money side is planned with the same care as the design.

The homeowners who feel most in control usually stop treating financing like the last step. They treat it like part of the design. If you’re building savings slowly, it helps to understand what is a sinking fund so you can set aside money for cabinets, labor, and the unknowns that show up during construction. That mindset keeps the project grounded in reality instead of wishful numbers pulled from an online calculator.

A lot of the stress also starts with inspiration. Homeowners save beautiful kitchens online, then run into the gap between photos and real project costs. If that sounds familiar, this look at Pinterest kitchen inspiration vs reality in Cherry Hill is a useful reminder that good planning starts with what fits your house, your neighborhood, and your budget.

Table of Contents

- Your Dream Kitchen and The Reality of The Budget

- Accurately Estimating Your South Jersey Remodel Costs

- Comparing Your Top Kitchen Remodel Finance Options

- Applying for Financing and Avoiding Common Pitfalls

- Coordinating Your Payments and Project Timeline

- Let The Cabinet Coach Simplify Your Budget and Design

Your Dream Kitchen and The Reality of The Budget

A common South Jersey scenario looks like this. A family buys a solid older home for the neighborhood, lives with the kitchen for a few years, and finally decides they can’t keep fighting the layout. The cabinets are worn, storage is poor, the lighting is bad, and the room still reflects choices made decades ago.

Then the budgeting starts.

At first, many homeowners think the challenge is finding the right finish or deciding between painted and stained cabinetry. It usually isn’t. The actual challenge is aligning the dream with what the house supports, what the neighborhood supports, and what the household budget can carry comfortably for years after the project is finished.

That’s where kitchen remodel finance becomes practical instead of intimidating. Financing isn’t just borrowing money. It’s deciding whether the project should stay cosmetic, whether to refinish or replace, whether the wall you want to move is worth the disruption, and whether the payoff is daily function, resale value, or both.

Most kitchen budget problems don’t start during construction. They start when homeowners commit to a scope before they’ve priced the real work.

In Camden and Burlington Counties, that matters because two kitchens can look similar online and cost very differently in real houses. One may be a straightforward cabinet and surface update. The other may involve electrical changes, floor leveling, ventilation corrections, or structural surprises after demolition.

The healthiest starting point is to ask simple questions.

- What bothers you every day: poor storage, bad flow, worn finishes, or lack of seating?

- What are you trying to protect: monthly cash flow, home equity, or a timeline tied to a move?

- What kind of house is this: forever home, five-year home, or resale project?

When those answers are clear, financing stops feeling like a barrier. It becomes the tool that shapes a smarter project.

Accurately Estimating Your South Jersey Remodel Costs

A Medford or Haddonfield kitchen can fool you on paper. The room may look like a simple cabinet swap, then the walls come open and you find old wiring, patched plumbing, an out-of-level floor, or a soffit hiding ductwork that limits the layout.

That is why a useful budget starts with your actual house, not a national average.

If you are still deciding whether to keep the cabinet boxes and update the fronts or replace everything, this guide to the cost of kitchen cabinet refacing helps narrow one of the biggest cost decisions early.

What a real kitchen budget includes

In most South Jersey remodels, the final number is shaped less by one dramatic finish choice and more by scope discipline. Cabinetry usually sets the direction. Labor, electrical work, plumbing adjustments, countertops, flooring transitions, and finish details push the budget into its real range.

A solid estimate should separate the project into clear buckets so you can see where the money is going and where the risk sits.

| Budget area | What it covers | Why it matters |

|---|---|---|

| Cabinetry | boxes, doors, hardware, organizers, trim panels | Usually the largest visual and functional decision |

| Labor | demolition, installation, carpentry, painting, trade coordination | Older homes raise this cost quickly |

| Surfaces and fixtures | countertops, sink, faucet, backsplash, lighting, flooring touch-up | These items affect daily use and finish quality |

| Mechanical updates | electrical, plumbing, ventilation adjustments | Often required once the layout or appliances change |

| Contingency | concealed conditions and mid-project corrections | Keeps one surprise from breaking the whole budget |

Homeowners often underbudget the parts they do not see in Instagram photos. Filler strips, crown details, outlet relocation, drywall repair, permit costs, appliance lead times, and temporary kitchen workarounds all have real dollars attached.

Before you sign anything, make sure the proposal spells out the elements of contract clearly. That matters just as much as the bottom-line price, because vague scope is where budget overruns start.

Why older South Jersey homes need contingency money

In Camden and Burlington Counties, contingency money is not a nice extra. It is protection against the kind of conditions we see all the time in houses built decades before modern kitchen loads and layouts.

A ranch in Cherry Hill may need dedicated circuits once new appliances are specified. A Collingswood home may have plaster, uneven framing, or older plumbing routes that turn a simple sink move into a larger trade job. In Moorestown and Haddon Township, I have seen floors that look fine until cabinet lines make the slope obvious.

A practical allowance for unknowns keeps those discoveries from stopping the project midway.

Use a larger contingency if the remodel includes any of the following:

- moving walls

- relocating plumbing or gas lines

- adding recessed lighting or under-cabinet lighting

- replacing old flooring under the cabinet footprint

- correcting ventilation for an over-the-range hood

- working in a home with known electrical or structural age issues

If the house is older and the work touches walls, wiring, or plumbing, the first estimate should be treated as a planning number until demolition confirms conditions.

How scope affects return in the South Jersey market

South Jersey resale value is local. A kitchen that makes sense in a higher-end pocket of Moorestown may be overbuilt for another block in Pennsauken or Lindenwold. The goal is not to spend as much as possible. The goal is to improve function and appearance to a level the house and neighborhood can support.

The National Association of Realtors reports that kitchen upgrades are among the projects buyers notice most, especially when the work improves livability instead of chasing luxury for its own sake, as outlined in its Remodeling Impact Report. That lines up with what sells well here. Better storage, cleaner cabinet lines, durable counters, updated lighting, and practical appliance choices usually land better than a full luxury redesign in a mid-range neighborhood.

For many homeowners in Camden and Burlington Counties, the strongest budget choices look like this:

- Smart spending: cabinet upgrades, drawer storage, lighting, counters, sink and faucet improvements

- Use caution: major structural changes, highly personal finishes, premium appliances that outprice the neighborhood

- Best resale balance: a mid-range remodel that fixes daily problems and looks current without forcing top-of-market pricing expectations

A good estimate answers one question clearly. Are you paying for work that improves how the kitchen functions and what the house is worth, or are you paying for scope that feels impressive but does not hold up in your market?

Comparing Your Top Kitchen Remodel Finance Options

A Medford or Cherry Hill homeowner might have a solid kitchen plan on paper, then hit the harder question. How should this be paid for without straining the household six months from now?

In Camden and Burlington Counties, that answer usually depends on three things. The age of the home, the amount of equity available, and whether the remodel is a contained cabinet-and-counter project or the kind of job that starts exposing wiring, plumbing, and wall issues once work begins. A 1960s split in Marlton and a century home in Haddonfield do not carry the same financing risk, even if the kitchens look similar at first glance.

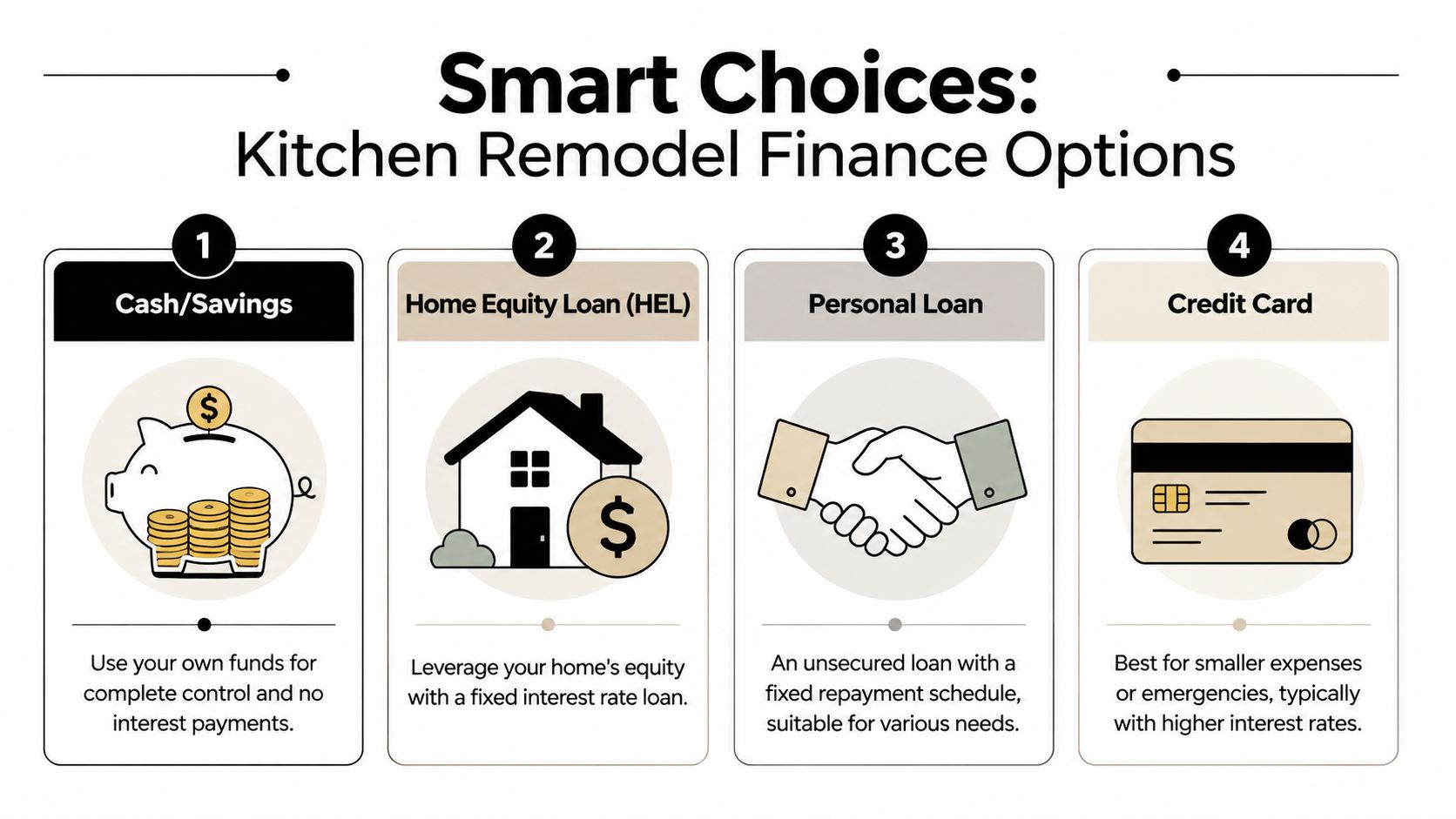

Cash and savings

Cash is still the simplest way to fund a remodel if using it does not wipe out your reserves. There is no lender approval, no interest cost, and no waiting on bank timelines while cabinet orders and installation dates are being scheduled.

It fits best for smaller or more controlled projects. Cabinet refacing, stock or semi-custom cabinet replacement, new counters, lighting, and appliance swaps are common examples.

The caution is straightforward. Older South Jersey homes can produce surprise costs fast. If a cash-funded remodel leaves you with little left for a panel upgrade, subfloor repair, or plumbing correction, the cheaper option on paper can become the riskier one at home.

Home equity loan and HELOC

For homeowners who have built equity, these are often the strongest options for larger kitchen remodels. They usually carry lower rates than unsecured borrowing because the home backs the loan.

A home equity loan is better for a tightly defined project with a fixed contract amount. You receive one lump sum and make predictable payments. A HELOC works better when the draw schedule may need flexibility, especially if the project is being completed in phases or if you want some room for conditions found after demolition.

That flexibility has a trade-off. Variable payment structures can be harder to manage if rates change or if the project drifts beyond the original scope. Your house is also tied to the loan, so I usually tell homeowners to be honest about monthly comfort, not just approval amount.

If you are comparing equity-based borrowing options, the EHF Mortgages remortgage guide gives a useful plain-language overview of how homeowners evaluate releasing equity. It is written for a different lending system, but the core questions still apply.

| Option | Best for | Main advantage | Main caution |

|---|---|---|---|

| Home equity loan | Fixed scope and contract price | Stable monthly payment | Home is collateral |

| HELOC | Phased work or flexible draw timing | Access funds as needed | Payment cost can shift |

Personal loans and credit cards

Personal loans make sense for mid-range kitchen projects where the budget is clear and the homeowner wants fixed payments without putting the house up as collateral. Approval can also move faster than equity lending, which helps when a homeowner wants to keep the project schedule tight.

They are less forgiving if the scope is still changing. If the remodel may grow once walls open up, a fixed personal loan can leave too little room.

Credit cards are best kept on a short leash. They can work for a single appliance, a deposit you plan to clear quickly, or a small overage. They are usually a poor foundation for the main remodel budget because revolving interest can erase any pricing advantage from the project itself.

Contractor financing and second-look options

Contractor financing can be a practical fit if you want the design, estimate, and financing discussion tied together. That often reduces confusion because the numbers being financed are connected to the actual scope instead of a rough guess.

One example is the The Cabinet Coach financing page, which explains available financing access through Wisetack and Acorn Financing. For homeowners comparing cabinetry, layout changes, and payment options at the same time, that setup can make the process easier to manage.

Second-look financing is also worth asking about if a prime lender says no. Declines happen for reasons that do not always reflect whether the remodel is sensible. Self-employment income, a recent job change, higher credit utilization, or an old credit issue can shut down one option while another lender may still approve the project under different terms.

That is important in practice. A declined HELOC or personal loan application does not automatically mean the kitchen has to wait a year.

Use these decision cues as a starting point:

- Choose savings for smaller projects if you can keep a healthy reserve after the work is done.

- Choose a home equity product for larger remodels with strong equity and a payment you can comfortably carry.

- Choose a personal loan if you want fixed terms and do not want the home tied to the financing.

- Use credit cards sparingly for short-term or limited purchases, not the main contract amount.

- Ask about second-look programs if the first approval does not come through.

The right financing choice should still feel manageable after the kitchen is finished, the final invoice is paid, and the monthly payments become part of regular life.

Applying for Financing and Avoiding Common Pitfalls

The application process is where a lot of homeowners either protect the project or undermine it. A lender, financing partner, or contractor program can only underwrite what’s in front of them. If your numbers are loose, your scope is fuzzy, or your paperwork is incomplete, the financing gets harder and the remodel gets riskier.

Verified planning data from Realm Home’s renovation budget guide shows 78% of renovations exceed their initial budgets, often because homeowners rush planning and don’t secure a fixed-price contract. That number should change how you approach the paperwork. Financing should follow a well-built estimate, not guesswork.

What lenders and financing partners want to see

Strong applications usually have the same ingredients. They show that the homeowner knows the scope, understands the payment obligation, and has contractor documentation that supports the request.

Bring these items together before applying:

- Income records: pay stubs, tax returns, or other standard proof of income

- Debt picture: current obligations and monthly payment awareness

- Project estimate: a written breakdown, not a verbal ballpark

- Property details: enough information for equity-based lending if that’s your route

- Contingency thinking: evidence that you’re not financing to the exact penny

A vague estimate makes everyone nervous. A detailed one helps. That’s especially true in older South Jersey homes where scope can shift after demolition if the planning was rushed.

A lender can finance a project. They can’t fix a poorly defined project.

The contract details that protect your budget

Financing approval is only half the battle. The contract controls what happens after approval.

If you want a simple refresher on the legal basics, this overview of the elements of contract is useful background. In practice, for remodeling, homeowners should focus less on legal vocabulary and more on whether the agreement clearly states scope, payment timing, allowances, and change-order procedures.

The economic side of remodeling matters too. This article on navigating kitchen and bathroom remodeling in the current economy is a helpful reminder that uncertainty in materials and labor makes clear documentation even more important.

A fixed-price structure, when appropriate for the project, helps reduce drift. So does itemized language. “Kitchen remodel” is too broad. “Remove existing cabinetry, install specified cabinets, complete listed electrical revisions, install selected countertops and backsplash” is much safer.

Here’s a good filter for any agreement:

| Contract point | What to look for |

|---|---|

| Scope detail | Specific work listed in writing |

| Payment terms | Linked to milestones, not vague dates |

| Allowance clarity | Clear note of what products are included |

| Change orders | Written approval before added work proceeds |

A rushed application often leads to a rushed contract. That’s exactly how homeowners finance one kitchen and end up paying for another.

This short video is a good companion if you want to think through financing choices before you sign anything.

Coordinating Your Payments and Project Timeline

A financing approval doesn’t make a project run smoothly. Payment timing does.

Many homeowners assume that once the money is available, the hard part is over. In practice, the project stays healthiest when payments match visible progress. That keeps the contractor funded appropriately, keeps the homeowner informed, and reduces the chance that money gets disconnected from the actual work.

![]()

![]()

Verified homeowner sentiment from the NARI 2025 Remodeling Impact Report shows that kitchen remodels score a perfect 10/10 Joy Score, which tells you something important. People love the result. But that satisfaction depends heavily on whether the path to completion feels organized rather than chaotic.

Match payments to real milestones

The cleanest remodels usually follow a milestone logic. Not every contractor structures payments the same way, but the principle should be the same. Pay against progress.

A healthy payment rhythm often includes:

- Initial deposit: secures design work, scheduling, and product ordering

- Post-demolition or rough phase payment: tied to early execution milestones

- Cabinet or material delivery payment: linked to major goods arriving

- Substantial completion or final payment: released when punch-list items are addressed according to the agreement

This project planning guide on how to plan a kitchen remodel is a useful reference point because it reinforces how scheduling, selections, and trade coordination affect when money needs to move.

Don’t let the payment schedule float separately from the schedule of work. Those two documents should tell the same story.

Handle changes without losing control

Change orders are where good budgets wobble. Some are necessary. Once walls open, you may need to correct wiring, address framing, or adjust a product choice because a lead time changes. The problem isn’t change itself. The problem is undocumented change.

Use a simple discipline:

- Pause before approving extras. Ask whether the change is necessary, elective, or cosmetic.

- Get the price in writing. No hallway conversations, no memory-based approvals.

- Decide where the money comes from. Contingency, savings, or a reduction elsewhere.

- Track the timeline impact. Added work often affects more than cost.

That’s how you preserve control. It’s also how you protect the emotional side of the project. A kitchen should feel rewarding at the end, not financially sour because the payment plan was vague and every change felt like a surprise.

Let The Cabinet Coach Simplify Your Budget and Design

A lot of financing stress starts long before a lender reviews an application. It starts when a South Jersey homeowner has a rough wish list, a few inspiration photos, and no clear agreement on what the project includes.

That gap gets expensive fast in Camden and Burlington County, especially in older homes where kitchen walls are rarely square, electrical service may need attention, and standard cabinet layouts do not always fit the room cleanly. A budget works better when the design is tied to the house itself, the neighborhood, and the resale expectations for that part of the market.

The Cabinet Coach brings those decisions together early. Homeowners can sort through cabinetry, countertops, hardware, tile, and layout choices before locking themselves into a financing number that may be too low or aimed at the wrong priorities. You can see how that planning process works in The Cabinet Coach experience.

That structure helps in practical ways:

- Scope gets clearer early. Cleaner scope usually means fewer financing revisions and fewer surprises once pricing is finalized.

- Spending stays focused on visible, durable improvements. In this market, cabinetry, counters, layout function, and storage usually carry more weight than scattered add-ons.

- Older-home problems show up sooner. That gives homeowners time to decide whether to use contingency funds, adjust selections, or phase certain work.

I’ve seen the same pattern over and over in South Jersey kitchens. Homeowners who make product and layout decisions early tend to have a steadier project. Homeowners who finance first and define the job later often end up adjusting scope midstream, which is where budgets start to slip.

Kitchen remodel finance gets simpler when the estimate matches the actual job, the design fits the house, and the investment is aimed at improvements that hold value in our local market.

If you’re planning a kitchen in South Jersey and want help turning early ideas into a workable budget, start with The Cabinet Coach. Clear design decisions and a well-built estimate can make the financing side of the project much easier to handle.